Vedant Fashion IPO: Will it fit well in your portfolio?

Vedant Fashion (of Manyavar fame!) has launched its IPO. But will it fit well in your portfolio? I explore this and more

Indians, festivals & celebration! It is not possible to think one without the other two. And why not when India is home to over 33 million gods. Add to that weddings and other family functions where towns are painted red. And right in the middle of this is the INR 5.6 (as of FY20) trillion Apparel market slated to grow over CAGR 18% by FY25. 32% Ethic Wear & 18% wedding & celebration wear forms the lion’s share in this Apparel market. After all what’s celebration if you are not looking & feeling better?

Vedant Fashion Ltd. (owner of the popular Manyavar brand) a category leader in the branded segment in wedding & celebration market is now going public on Indian bourses. Being a fairly regular customer, I wanted to get a sense if there is any juice in its IPO issue!

I have always felt that if you start with the qualitative story and if its woven with care you will love it by the time you reach the numbers (read financial statements). We are humans, and salve to our emotions (alas). So, I would first want to go looking at the numbers, hoping to decipher something worthwhile.

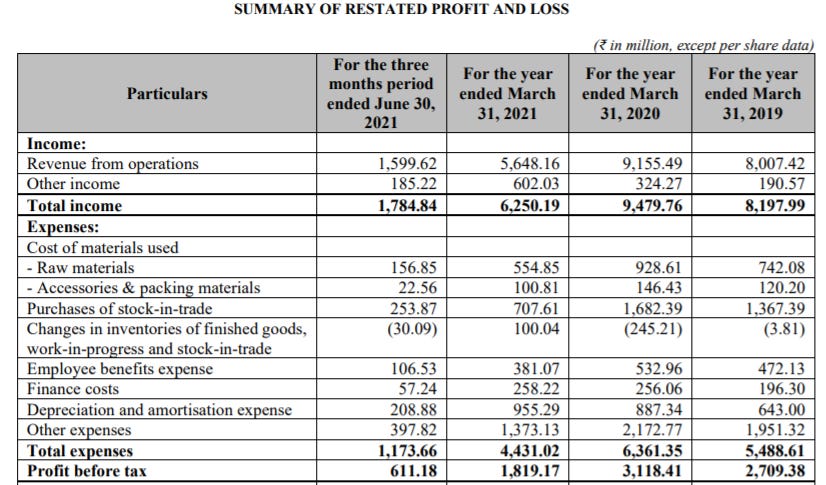

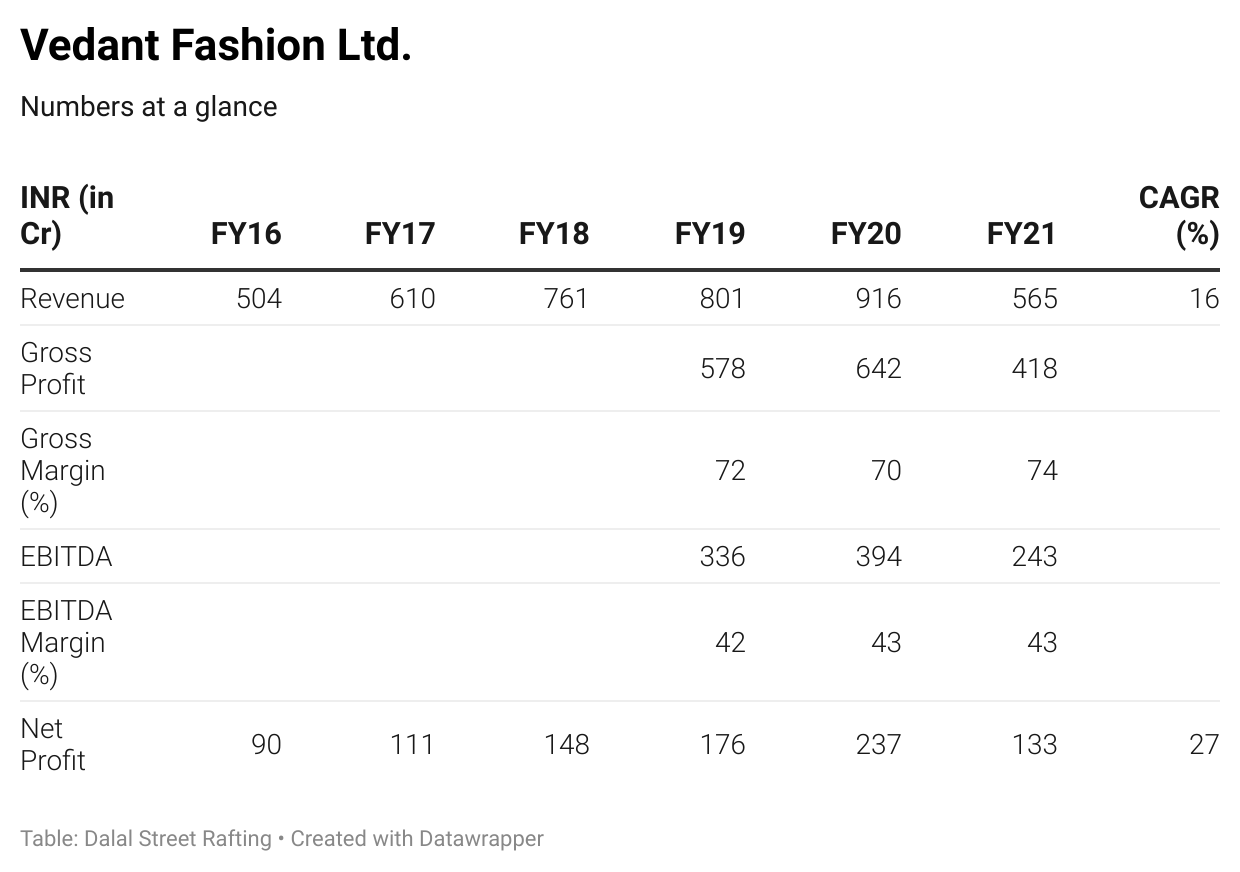

Gross Profit for FY19, FY20 & FY21 stands at 72.2%, 70.2% & 74.1% and corresponding EBITDA margins are 41.9%, 43% & 43% ! It is not every day that one sees companies making such fat margins. Vedant Fashion (from investing point of view) certainly has my attention.

If you ever scoffed at any Manyavar billing counter, after being told that they never offer discount, you can now see that they were being brutally honest. If I place its closest listed peers TCNS Clothing & Aditya Birla Fashion for a comparison, both give way to Vedant’s dominance convincingly. If we take FY20 as the year for comparison (given the FY21 had been a one-off year with lockdowns & restrictions) TCNS & Aditya Birla Fashion did EBITDA Margins of 16.2% & 14.6% (compared to Vedant’s 43%).

It is interesting to note that TCNS revenue grew at a faster rate CAGR 24.1% (FY16-20) compared to Vedant’s 16.1%. Given TCNS’s discount led sales led this growth as against strict pricing policy and branding of Vedant, the growth of this IPO bound company feels much better (Aditya Birla Fashion isn’t even in the question with CAGR of 9.7%).

Before we move on from its Profit & Loss statement it worthwhile to mention that it has done a commendable job on the cost side too. It has consistently maintained its employee cost (as % of sales) between 5.9% & 6.7% and other expenses between 24.4% & 24.3% for the FY19-21 period.

With zero debt, and market cap of nearly INR 20,000 Cr an ROE of 22.2 (FY20) is fairly respectable for a business.

Clearly a great business just by looking at the numbers. Now could be a good time to take a step back, and get a larger industry context and view Vedant through the lens of a qualitative prism.

The IPO prospectus mentions the branded space is expected to grow at a CAGR of 18-20% by FY25. Expenditures around celebration tends to be looked at as once a year or once a lifetime events (like weddings). As a result such products have a natural pricing power. Price tags, for a change, is not the top most thing on the mind of Indians who are very price sensitive otherwise. Borrowing from the CRISIL research which is quoted in the DRHP about 9.5 - 10 millions wedding will happen per year in India. Clearly the industry is good too.

So good that many firms have started getting attracted towards it. We have spoken on TCNS clothing, but other prominent & growing company includes Soch Apparels, Jadeblue Lifestyles, Ritu Kumar label, and another IPO inbound name - BIBA among others. Recently the behemoth - Reliance Industries’ fashion arm has shown keen interest in the space and has acquired 40% of well know celebrity designer Manish Malhotra’s brand along with few other acquisitions. So competition is clearly getting hotter in the space.

Having said that Vedant has been successful in making a space for itself. It had the advantage of seeing this market opportunity early on (it started in 2002) and used correct strategies along the way. Apart from the flagship brand Manyavar (mid-premium brand) it is moving strongly in both value segment (Manthan) & premium segment (Twamev). It has also made careful acquisition like Mebaz (a brand with wide presence in Southern India) to enhance it market share.

Its has full control on the supply chain and high quality checks & measures in place. For retail distribution it has 3 approaches. 88% of the sales are made at Exclusive Brand outlets (EBO). These EBOs are majorly franchise owned, making it a asset light model. I am now beginning to see why the ROE was better. Rest 8% revenue comes through the Multi Brand outlet (MBO) and remaining customers make purchases through e-commerce. EBOs are instrumental in providing a premium experiential feel which is beneficial in cross & upselling.

If you are still on this article, you can judge me that I am getting all rosy with the business and industry. And, I think you are right too!. It is hitting on all the right places where I look before putting my money in. But now is time to see how this IPO issue is priced and a great time to share one of my all time favorite quotes from the legendary Warren Buffet.

Price is what you pay, Value is what you get

The company is valuing itself at INR 21,017 Crores. The IPO size is INR 3,150 Cr. At INR 866 per share (upper end of the price band). So if I have to break down, it means for every Rupee of profit made by the company (IN FY20), its asking from investors INR 90 (i.e PE ratio). At an EPS of FY21 PE is 159, although like for almost most part of the article I am using FY20 for comparison. All the good feeling that gathered on me seems to be abandoning me right now! I now need to look for what the proceeds of this IPO be used for.

So this IPO is an 100% Offer for Sale. 47.8% of the IPO sale proceeds will be going to a Private Equity investor - Rhine Holding, 1.98% to another PE Kedarra Capital (making a complete exit) and 49.72% to promoters who are also partially liquidating their stake. Just for my personal curiosity little digging led me to find that both the PE firms has an average acquisition cost of INR 166.27 share. (421% returns!)

The Profit CAGR for the period FY16-20 is ~27.3%. At PE of ~90 (EPS FY20) this pricing has gone quite overboard and seems to have not taken many risks into account like newer competition, inability to maintain the brand leadership and pricing power or changes in styling preferences that might evolve over time.

Yes, this is an amazing business. And yes, I am adding it to my watchlist for better entry levels, but at this price - Yeh meri expertise nahi hai, I am out!

If you have stayed this long and feel this article was worth your valuable time please subscribe to Dalal Street Rafting - my new publishing on Substack, and share it with your friends & colleagues!

Disclaimer: Views presented in this article is personal opinion of author and doesn’t not represent any firm’s view that he is currently associated or might have been associated in the past. No part of it should not be considered as a recommendation to buy or sell any stocks etc. This is an educational article and although care has been taken for correctness of the data, author does not take any responsibility for any errors or omissions.