Navi Technologies: Can it break tech IPO's bad patch?

Navi Technologies: Can it break tech IPO's bad patch?

Navi Technologies got nod for it INR 3,350 Crores IPO from regulator, amidst media & analyst’s critical commentary on release of much delayed financials of Byju’s & Oyo filing fresh docs for IPO after claiming maiden EBITDA positive quarter. Navi caught my attention especially because not too far back in May 2022 its micro finance entity application for universal private bank & SFB (small finance bank) was rejected by RBI. Which many believed would act as speed-breaker to its IPO.

I decided to devour Navi Technologies prospectus in search of cues if its business & financials were worth the hype that surrounded it ever since its launch. Much of which was due to its star founder & promoter Sachin Bansal, who started Navi after exiting his first startup - Flipkart.

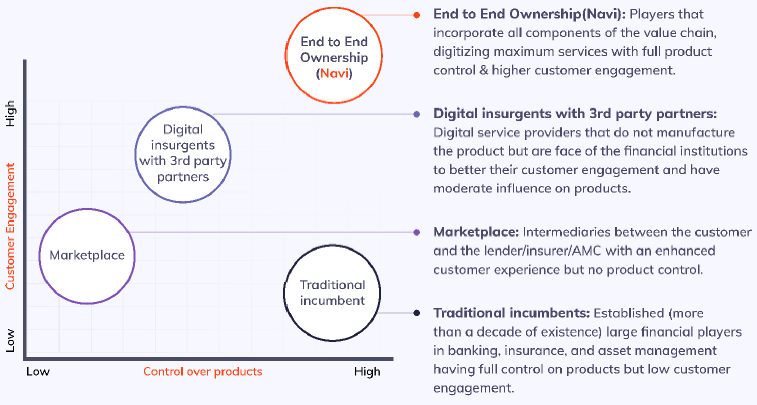

Navi, a home grown fintech firm offers 3 non-payment financial offerings - lending, insurance & asset management. It is a first of its kind to list on Indian bourses. While not a peer, Paytm bears minor resemblances with Navi - they both offer insurance, wealth management & lending. But with a major difference. Navi does all of them from its own balance sheet and is not merely a distributor like Paytm or majority non-listed fintech players. The complete control over both product & customer engagement offers Navi its unique strength. Especially when most fintech players in their endeavor to stay asset light are opting merely to be aggregators & distributors.

Barring its digital lending business (personal & home loans) Navi followed the path of acquisition for its other businesses. Like acquiring DHFL General Insurance in February 2020, Essel Asset Management Company in February 2021 & Chaitanya India Fin Credit which provides micro finance loans in March 2020. The revenue share from each business (for 9 months ended Dec, 2021) gives a fair idea which business has what weight to move the needle for Navi.

Digital Lending

Personal loans was the first segment with which Navi launched its operation in April 2020. With a digital only process through Navi App, instant personal loans up to INR 20 lakhs are being offered for tenors up to 7 years. During the 9 months ending December 31, 2021

No. of personal disbursed: 3,08,383

Closing AUM: INR 1418.6 Cr

Average ticket size: INR 50,990

Average Tenor of loans: 21.99 months

The key differentiator being the all digital process leads to a TAT (turn around time) of 5 mins within which proceeds of loan amount is received in user’s bank account. This compares to 1-3 days that current players take after the loan enquiry with countless paperwork & office visits in middle.

Extending this business, Home loan was launched in February 2021. Offering loans up to INR 10 Cr for tenor of up to 30 years and interest rate beginning from 6.4% . TAT for pre-approved projects are 1-2 days with the eligibility offer being given through a completely automated process, not requiring any manual checks. Since launch:

No. of personal disbursed: 604

Closing AUM: INR 177.7 Cr

Average ticket size: INR 38.6 Lakh

For all the products within digital lending Navi claims leveraging their machine learning based under writing models. Arming it process loan request at such a lighting speed. Also, cross selling opportunities are being grabbed by both hands. For instance 71.69% of all home loans customers were from Navi’s personal loan user base.

Microfinance Lending

Through subsidiary Chaitanya India Fin Credit, Navi provides credit to low-income women in rural & semi-rural areas across India. The model adopted by Navi is joint liability group lending model, where a small number of women form a group and guarantee one another’s loan.

These loans are not offered on the Navi App. And given the customer base of micro finance loans are very different from customers availing digital lending, there isn’t much opportunity of cross selling either. The core value proposition & key differentiator of full digital, seamless process with low TAT is lost. Then why this business you may ask?

It could be because Navi believes this the path of least resistance for universal banking license. While RBI has rejected its application this time, it can continue re-attempting.

Insurance

Like lending, Navi’s core value proposition in Insurance business is an all digital process with shortest possible TAT, of the order of less than 2.5 minutes! Navi offers wide range of insurance products - health, motor, fire, personal accident etc.

Navi leverages diverse set of data variables (financial profile, lifestyle, family history etc.) to asses & price risk better for the premiums sold. Cross sell opportunities have shown promising results in this segment as well with 52.67% of all retail health insurance customers were from Personal Loan interested user base.

Asset Management

The newest kid for Navi, Navi Asset Management (AMC) started its operation only in Q1FY22. Its a passive focused AUM. During the 9 months ending December 2021 ~70% of the net inflow came from passive funds. So much so that I was unable to find any active fund on their website even though their DRHP mentions 4 active Equity fund with closing AUM of 524.7 Crs.

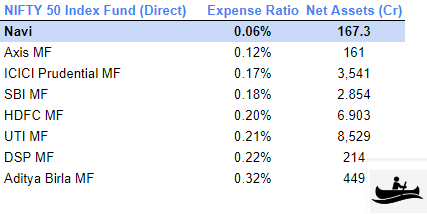

The value proposition being low expense ratio, managing tracking error & creation of strong brand in passive investing. The biggest passive fund of Navi’s - Nifty 50 Index Fund has perhaps the lowest expense ratio of 0.06%

Navi claims to have extensive trading systems & technology platforms to assist the in-house research team for opportunity identification & well designed process to keep tracking error & expense ratio low.

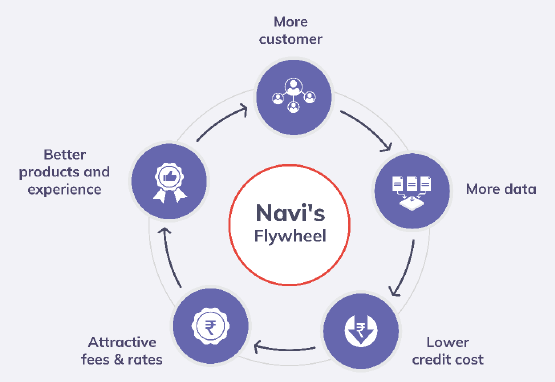

Navi’s Flywheel

Across its businesses, Navi is relying on the same flywheel - gathering data from customer which helps its machine learning based underwriting models price the risks more accurately thereby giving attractive fees & rates compared to any other competitors. Supplemented by better products & experience more customers & transactions happen on the Navi App leading to more data generation.

All of it sounds perfect in theory except that financials doesn’t indicate this flywheel wheel kicking in, at least not yet.

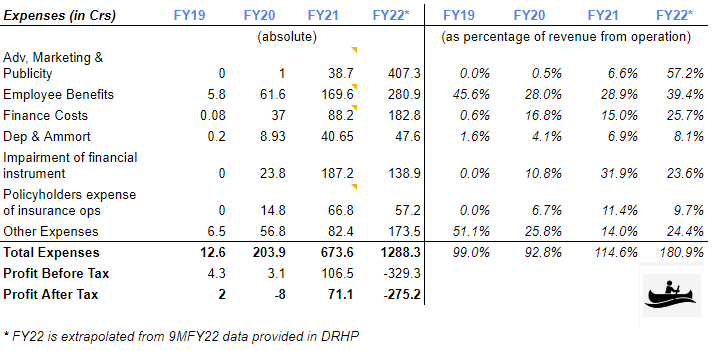

Financials - revenue moving in tandem with costs

While income number themselves don’t paint very sorry state, growth in them have to be taken with a pinch of salt.

Net gain on fair value changes refers to net gain on debt securities on trading portfolio & net gains on futures trading. Net gain on derecognition of financial instruments is due to sale of loan portfolio through assignment.

Like insurance business had only 55 days of operation in FY20 so the increase in revenue next year was partly due to full year of operation, which is a normal business outcome. AMC business was operational only from Q1FY22. Home loans within digital lending also came online in February 2021 thus any meaningful contribution reflects only in FY22. With that being said the revenue doesn’t look that bad relative to other Fintechs both in listed or unlisted space.

All the businesses have established revenue model with only AMC business having to prove its profitability given its focused on passive instrument which have margins thinner than wafer.

The fact that flywheel hasn’t kicked in just yet for Navi is more pronounced when one looks at the expense side of P&L.

Navi’s advertising expenses especially over online platforms has zoomed up significantly in FY22. Expansion of lending & insurance business needed more employees along with expansion of tech team. Even if the flywheel does kick in at some point in time, it will only be after some stabilization of these business verticals.

Till then cost will be increase in tandem or at times even more than corresponding increase in revenue as newer cost heads gets introduced. For example customer onboarding & verification and rental charges under other expenses shows up in FY22 which was absent earlier.

Machine Learning models: will it stand test of time?

Navi’s machine learning models which is another core piece for Navi’s flywheel has yet to prove itself. Significant portion of the loan portfolio is relatively new and was disbursed only in last 8 months. Risks of delinquency in loans usually emerge from 4 to 12 months from disbursement. So how well these models are doing their work in predicting the risk and pricing them will show up only in few more quarters ahead. Concluding models are doing a fine job looking at current NPAs would be jumping the gun.

No PE & stake sale like usual tech Startup IPOs

Sachin Bansal, the promoter of Navi Technologies holds 97.77% of Equity share capital. In absence of PE players or any other significant shareholders it is only logical to expect that there wouldn’t be any stake sale. Except of course Sachin himself wants to partially exit which is not the case with this IPO.

Objective of the INR 3,350 Cr that is expected to be raised through IPO:

INR 2,370 for augmenting capital base of Navi Finserv, the non-deposit taking lender to personal & home loan business of Navi

INR 150 Cr for maintaining the current solvency level of Navi General Insurance

INR 830 Cr balance will most likely be used for general corporate purpose.

To me this is a green flag. In absence of PE’s pressure for growth (so as to make a timely exit) Sachin will have single minded focus to drive the company towards sustainable growth with controlled expenses leading to a profitable phase sooner than later.

The long & short of it

While prospectus mentions Navi is on track to achieve positive unit economics, I can’t guess with a reasonable accuracy how many years it would take to do so. The core piece is for the flywheel to move the way it is expected to. And with almost all the businesses still in their infancy it will take a while for it to kick in (given it does at sometime eventually).

Most new age Startups have spoken about how user data & ML models will help their case but only in due time it will known how well they have done what they are promising to. For Navi will be no different.

Speaking within the sphere of Fintech IPOs that have come or are in talks to hit markets in near future Navi has unique strengths (like lending from own balance sheet) and not tinkering with established revenue model for most of its business. Its financials are showing some simmers of hope when compared to contemporaries.

But the largest part of applying to this IPO will be betting on ‘Sachin Bansal’ and how well you think he can drive both growth & profitability without compromising one for the other.

Hope you found this article thought provoking & interesting. If you missed reading Gold ETFs, SGBs or Digital Gold: Who is golden of them all? by Dalal Street Rafting check it out below.

Disclaimer: Views presented in this article is personal opinion of author and doesn’t not represent any firm’s view that he is currently associated or might have been associated in the past. No part of it should not be considered as a recommendation to buy or sell any stocks etc. This is an educational article at best. Although care has been taken for correctness of the data, author does not take any responsibility for any errors or omissions. Readers should consult their financial advisers before taking investment decision.