LIC IPO: Can the elephant dance?

LIC IPO: Can the elephant dance?

India's biggest & much awaited IPO is here. I try to explore if it's worth your & my money?

IPOs almost always have interesting twists & turns to it. But few in Indian markets has seen what Life Insurance Corporation of India (LIC) have witnessed which opens for subscription today as you read this. So, Shuru Se Shuru Kartein Hain (Let’s begin from the beginning, shall we)!

On a fairly active day of trading in July, 2019 at an institutional equities desk where I worked previously, a senior sales guy walks into the trading floor saying he has begun conversing with Funds (read institutional clients) about LIC IPO. He didn’t seem much enthused, understandably so. Because apart from the investment bank I worked in, 11 others were named bankers to this IPO issue (finally it had 10 bankers, my ex-employer stayed on)! While I had already read about few articles in media, I now knew for certainty that the size of this IPO would be one of its kind. Around similar time Saudi Aramco’s listing talks were hot in financial markets, and with its humongous size being the center of those talks I kept wondering what would that be of this government owned LIC - the largest insurance company of the country.

Next year in Union Budget of 2020 Finance Minister Nirmala Sitharaman announced LIC would go public. Government would sell part of their stake and make it a listed entity. Reasoning shared was that by doing so would discipline the company, and unlock its value. But more important was that fact that government needed to raise fund to bolster the growth plan that it has envisioned for the country keeping a close rein on fiscal deficit. No further details were divulged. In just couple of weeks of this global financial markets were underwater due to COVID, Indian markets being no different. With uncertainty all around, the IPO took a back seat. Requirement for funds increased significantly for government, as now it needed not just for accelerating the growth but also an added job of jump starting the economy which hit screeching brakes after nationwide lockdowns and widespread COVID cases across India. The desperation was clear in Union Budget 2022 where Sitaraman said the mega IPO offer was expected “shortly”. The divestment target was revised downward because government felt that if too high a target was kept, it would lead to distortion of the markets.

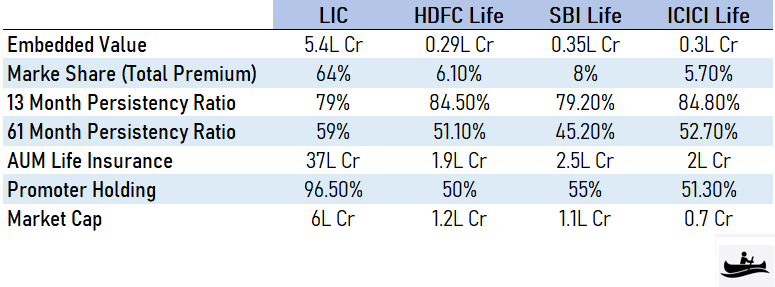

Embedded Value - Book Value cousin of Insurance Firm

I kept second guessing myself on how big the IPO would be. Until few days after the budget in February when the Embedded Value (EV) of the LIC was announced as Rs 5.4 Lakh Crores (Rs 5400 Bn). Embedded Value, for the non-analyst type reading, is a cousin of Book Value that is used for usual companies. What makes an insurance company unusual is the uniqueness of the core product - Life Insurance, where the revenue for the insurer comes from policies in place but cash flows are only realized in future when premiums are paid. At this point government was looking to sell 5% of its stake in the company.

Comparing the Embedded Values of LIC with its listed peers is an effective way to visualize the massive size that LIC has. Another metric of LIC which can awe any market observer is the Asset Under Management (AUM) which is defined as total value of shareholders’ & policy holders’ investment managed by the firm. LIC has an AUM of Rs 40.1L Cr (as of December 31, 2021). This is more than the entire domestic mutual fund industry of India.

While the EV cat was out of the hat, the valuation at this point still wasn’t. Insurance firms usually trade at some multiple of its EV. And this is where the Russia-Ukraine war played spoilsport adding to the already negative bias the foreign investor had on all Emerging Markets (including India) after rate hikes by US FED became imminent. The investor sentiment dampened. LIC and government had to cave in. LIC (& finance ministry) not only reduced the multiple, but also the stake they wanted to sell. Down to 3.5% from 5% the was initially planned.

The valuation angle

The valuation tussle was constantly on between what the government needed and what investors were willing to give LIC. Although that is normally what happens between every company going public and the prospective investor in its IPO, in LIC’s case this struggle lasted longer, became much more public (as it was government at one end after all) and gave market onlookers enough time to throw their views around. For the period FY16 to FY21 the total premium of LIC has only grown by CAGR of 9% compared CAGR of 18% by private life insurance players in India. But finally with the IPO being priced cheaper than it peers (at 1.1x its EV) there is definitely some valuation comfort in this IPO. And given the size & business stage in which LIC is at currently, it might not be fair to expect similar (or better) growth rates for LIC compared to its listed peers.

Why government restrained from pricing it exorbitantly? Increasing desperation to raise fund (as other avenues like hike in taxation on fuel etc. has been maxed out and began to push inflation beyond the comfort level) with increasingly deteriorating global market sentiment, government could have finally decided to keep the valuation at a more reasonable level. Any more wait would lead to revaluation of the Embedded Value (which is valid for next 5-6 months only from when its completed) which is a time consuming process and GoI (government of India) was running short of it. I also feel that government wants to leave some money on the table for the investor as they would likely be back sooner than later to divest some other GoI holdings (it could be another round of stake sale of LIC itself) ! And, they are not wanting to set a bad precedence.

With the stake sale size & valuation both locked, the size of the IPO comes to be Rs 20,557 Cr. I finally got my answer to what I had began wondering at my trading desk back in 2019. But, this number was certainly smaller that what government would have liked or I initially guessed it would be. And, given Paytm, which until now is the biggest IPO (Rs 18,000 Cr) Indian stock market has seen, was digested (read subscribed to) fully, there is little doubt that LIC IPO will have any problem sailing through. I was very skeptical if with the initial size (~65,000 Cr) that would have been possible. To put numbers into perspective a good and active day in National Stock Exchange (which commands ~90% share in Indian Equities market) sees around 60,000-65,000 Cr of turnover in cash (stocks) segment.

LIC is big, not just by its size alone but also its reach. India today has ~9 Crore demat accounts and ~1.85 Crore mutual fund investor. Compare this with LIC’s 29 Crore Policy holders. And LIC understands its strength of omni-channel distribution network. It has carved out a 10% reservation in its IPO for its policy holders from within the 35% total reservation for retail investor and another 5% for its employees. It has sweeten the deal by giving Rs 45 & Rs 60 discount per share discount to retail and policy holder respectively. This further sweetens the deal for the small private investor.

An accounting change and multifold jump in profits

LIC profit might jump multifold in the next 2-3 years. To understand this I need to take a step back to explain how the profits generated flow to shareholders. Life Insurance products can be divided in linked and non-linked product. Linked products deliver returns that are linked to the markets while non-linked products are not linked to markets. In the case of LIC almost it’s entire offerings are non-linked products (99.7%). Non-linked products are further divided into

Participating products - Policyholders shares the profits of insurance company

Non-Participating products - Policyholders does not share profits

For LIC the split between participating & non-participating is 60.9% & 39.1% respectively. Until September, 2021 LIC has a single fund called ‘Life Fund’ which transferred 5% fund to share holder’s fund. However the new surplus distribution added a positive twist to it. Life Fund will now be bifurcated into participating policy holder’s account & non-participating policy holder’s account. 100% of non-participating policy holder’s account would become part of shareholder’s fund, while in case of participating policy holder’s account 5% would be diverted to shareholders account which will gradually increase to 10% in next 3 years. Putting numbers beside each category:

Life Fund - Rs 36 Lakh Cr

Participating account - Rs 24.6 Lakh Cr

Non-Participating account - Rs 11.4 Lakh Cr.

Carrying out a back of an envelope calculation:

Pre September, 2021 treatment :

Shareholders Fund = 5% of Life Fund = 5% of 36L Cr = 1.8 L Cr

Post September, 2021 treatment:

Shareholder Fund = 10% of Participating (after 3 years) + 100% Non-Participating

Shareholder Fund = 10% of 24.6L Cr + 100% of 11.4L Cr = 13.86 L Cr

That’s over 7.5 times increase of shareholder’s fund just with a change over the previous way of accounting all other things remaining same.

Unique IPO brings along unique risks

A unique IPO that LIC is, it also bring along with itself some unique risks for investors which are best to be aware of rather than crying foul later.

To begin with every listed company needs to dilute its promoter holding to 75% in 3 years from being listed. But government inserted new rule in Securities Contracts (Regulation) Rules, 1957 which exempts any listed public sector Co. (like LIC!). So although the government has allayed the fear of investors that it might not sell more of its stake in future, at any point in time it can decide to do so. This has been seen repeatedly in Coal India especially when the perennially falling stock price has demonstrated some will to turn around. Since listing in 2010, Coal India is down by 46.14% ! Indian Railway Catering & Tourism Corp. (IRCTC) has bucked this trend but being 10 times smaller than LIC’s market cap it might not make for an apple to apple comparison.

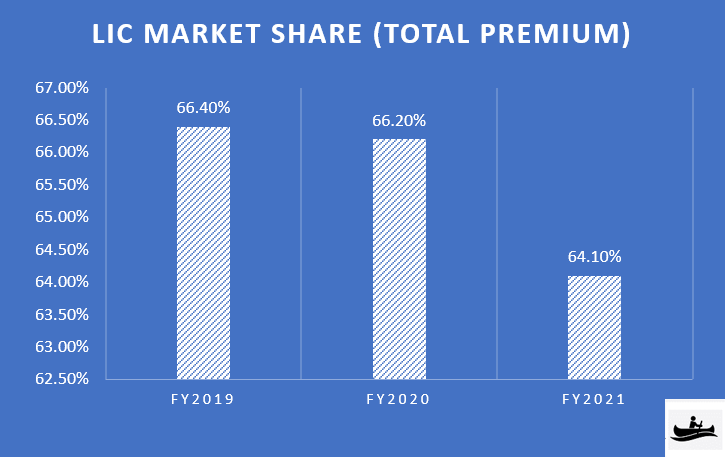

Another place that LIC finds itself in uncomfortable spot is that all of it’s competitors are private and have been growing much faster than it. These more nimble competitors have been able to chip away market share steadily from LIC.

Post listing government of India will continue to be the largest shareholder of the LIC. That would mean like in the past LIC might have to take action in line with government’s economic & policy objective which might not always be beneficial to it’s own business. A case in hand is when GoI in 2018 asked LIC to rescue debt ridden IDBI bank. LIC had to infuse Rs 4,743 Cr in the bank in exchange of 49.2% ownership. The banks financial conditions continues to be weak posing a risk for LIC. While search for a buyer is on, there has not been any luck yet. Such cases can repeat themselves in the future.

Worth my money?

While I acknowledge the risk, at this point the odds certainly look in my favor to apply in this IPO. The reasonable valuation looks more tempting when seen through the context of shareholders’ profit increasing multifold due to the accounting practice change. This could be a case of owning the business for less than it is worth. (Not an investment advice, read disclaimer below)

To me, you can love this IPO or hate it, but its too big to ignore it. And you shouldn’t ignore it!

Hope you found this article thought provoking & interesting. If you missed listening the podcast HIGH SIDE with Prakhar Gupta - Senior Investment Associate, GEF Capital Partners by Dalal Street Rafting check it out below. Now available also on Spotify (click here)!

Disclaimer: Views presented in this article is personal opinion of author and doesn’t not represent any firm’s view that he is currently associated or might have been associated in the past. No part of it should not be considered as a recommendation to buy or sell any stocks etc. This is an educational article at best. Although care has been taken for correctness of the data, author does not take any responsibility for any errors or omissions. Readers should consult their financial advisers before taking investment decision.